The Ultimate Tax Hack: Why Accredited Investors Are Flocking to Gas Stations in 2026

If you are an accredited investor looking to offset taxable income while generating reliable cash flow, traditional commercial real estate might not be working fast enough for you. Standard commercial buildings depreciate over a painfully slow 39-year schedule.

But what if you could write off a massive portion of your commercial real estate investment in the very first year of ownership?

Welcome to the world of gas station and convenience store (C-store) investing. Thanks to recent legislative changes — specifically the permanent return of 100% bonus depreciation — gas stations currently offer some of the most aggressive tax advantages in the real estate market.

Whether you are a seasoned commercial property owner or looking to make your first major real estate acquisition, here is what you need to know about utilizing gas stations as a powerful tax strategy.

What is Bonus Depreciation? (The 2026 Update)

In real estate, depreciation allows you to deduct the cost of an income-producing property over its “useful life,” lowering your taxable income. Bonus depreciation acts as an accelerant, allowing you to deduct a large percentage of eligible property costs upfront in the first year it is placed in service, rather than spreading it out over decades.

The Game Changer: The Tax Cuts and Jobs Act (TCJA) of 2017 originally introduced 100% bonus depreciation, but it began phasing out in 2023. However, with the passage of the One Big Beautiful Bill Act (OBBBA) in July 2025, 100% bonus depreciation was permanently restored for qualified properties acquired and placed in service after January 19, 2025.

This means that in 2026 and beyond, investors can immediately expense the full cost of eligible assets in year one.

The Gas Station Advantage: The 15-Year Rule

Bonus depreciation generally applies to assets with a class life of 20 years or less. Because standard commercial buildings have a 39-year life, the building itself usually doesn’t qualify for bonus depreciation.

Gas stations, however, are a massive exception. Under IRS rules, a gas station can be classified as a “Retail Motor Fuel Outlet.” If a property qualifies as a retail motor fuel outlet, the entire depreciable basis of the property (excluding the land) is classified as 15-year property. Because 15 years is less than 20 years, the whole building and its improvements become eligible for 100% bonus depreciation.

To qualify for this massive tax benefit, the property must meet just one of the following three IRS criteria:

| IRS Retail Motor Fuel Outlet Tests | Description |

|---|---|

| 1. The Revenue Test | 50% or more of the property’s gross revenues are generated from petroleum sales. |

| 2. The Floor Space Test | 50% or more of the property’s floor space is devoted to petroleum marketing sales. |

| 3. The Size Test | The convenience store building is 1,400 square feet or smaller. |

The Broker’s Reality Check

While the IRS gives you three ways to qualify, my advice to investors is to focus heavily on the first one: The Revenue Test.

Technically, a station can qualify just by being extremely small (The Size Test). However, in today’s highly competitive market, sub-1,400 square foot C-stores are often a relic of the past. As a broker, I generally advise my clients against purchasing these micro-footprint locations because they often lack the physical space needed to drive inside sales and survive long-term. You should never buy a dying business model just for a tax write-off.

Instead, the sweet spot for serious investors is the Revenue Test. The vast majority of the highly profitable, modern gas stations and expansive travel centers I broker easily pass this metric. Because fuel is a high-revenue product, a thriving gas station with a massive, highly profitable 5,000+ square foot convenience store will usually still generate more than 50% of its gross revenues directly from the pumps.

This allows you to acquire a robust, future-proof, large-format asset while still securing that 100% bonus depreciation.

What if the Property Doesn’t Meet the Test?

Even if you purchase a massive travel center or a gas station with a highly profitable, oversized C-store that fails all three tests, you are still in an incredibly strong position.

You can utilize a Cost Segregation Study. This is an engineering analysis that breaks down the property into its individual components. While the main shell of the building might remain on a 39-year schedule, a cost segregation study will identify assets that qualify for 5-, 7-, and 15-year depreciation schedules.

In a gas station, these highly depreciable assets are everywhere:

- Fuel pumps and underground storage tanks

- Pump canopies

- Specialized electrical and plumbing for the pumps

- Signage and security systems

- Parking lot paving and landscaping

Even without the 15-year building exception, a cost segregation study on a gas station can easily reclassify 25% to 40% (or more) of the purchase price into categories eligible for 100% bonus depreciation.

The Financial Impact: A Quick Scenario

Let’s look at how this plays out in the real world for an investor.

Part 1: The Base Math

- Purchase Price: $3,500,000 (Gas station & C-store)

- Land Value (Not Depreciable): $700,000

- Depreciable Basis: $2,800,000

If the property meets the Retail Motor Fuel Outlet test, the entire $2,800,000 depreciable basis is treated as 15-year property. Under current tax rules, you can apply 100% bonus depreciation. That means you take a $2,800,000 deduction against your taxable income in year one.

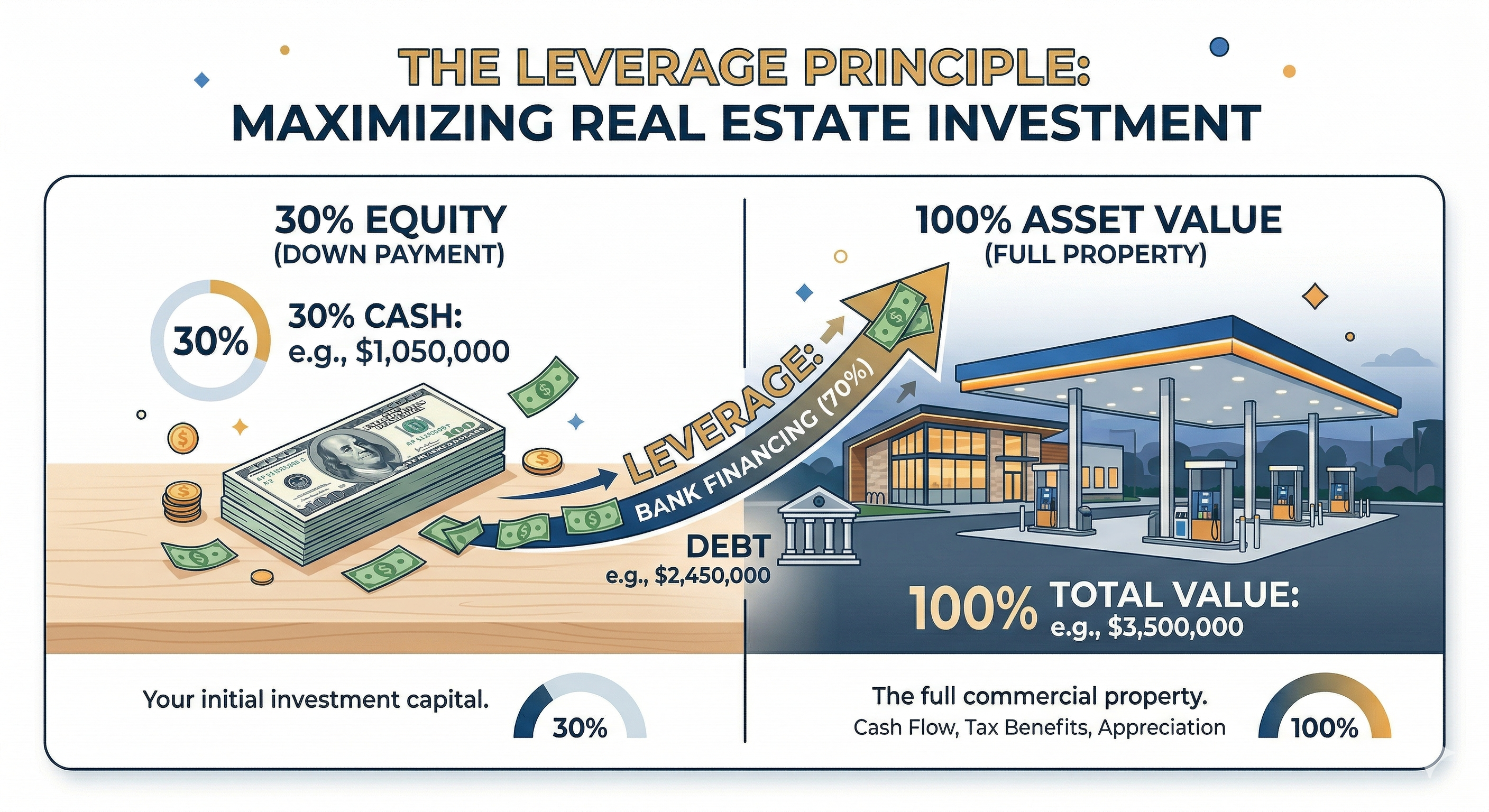

Part 2: The Power of Leverage (Depreciating the Bank’s Money)

Now, let’s take that exact same $3,500,000 property, but instead of paying all cash, you utilize leverage and finance 70% of the purchase using a conventional commercial mortgage, putting only 30% down.

Here is how the numbers break down:

- Purchase Price: $3,500,000

- Bank Financing (70%): $2,450,000

- Your Cash Down Payment (30%): $1,050,000

- Depreciable Basis (Building Value): $2,800,000

Here is the magic of commercial real estate tax law: Your depreciation deduction is based on the total purchase price of the asset, not just the cash you put into the deal. Even though you only brought $1,050,000 of your own cash to the closing table, you still get to claim the entire $2,800,000 bonus depreciation deduction in year one.

Because of the 100% bonus depreciation rules, your first-year tax write-off is more than double your out-of-pocket cash investment. Depending on your blended state and federal tax brackets, the actual tax savings generated by this single transaction could cover a massive portion of your initial down payment, effectively turbocharging your cash-on-cash return.

You keep the cash flow from the gas station’s operations, your tenants pay down the debt on the $2,450,000 mortgage, and you get a multimillion-dollar write-off on day one.

Note: Always consult with your CPA regarding debt basis, passive activity loss limitations, and your specific real estate professional status to ensure you can fully capture these losses against your active income.

Ready to Upgrade Your Portfolio?

Gas stations offer a rare intersection of recession-resistant cash flow, triple-net (NNN) lease stability, and unparalleled tax advantages. However, navigating the nuances of environmental compliance, brand contracts, and IRS tax qualifications requires specialized expertise.

As a commercial real estate broker specializing strictly in gas station properties, I know exactly what to look for to ensure a property is primed for maximum tax efficiency and operational success.

Don’t leave your capital tied up in slow-depreciating assets. Contact me today, and let’s find a gas station property that fits your investment goals and supercharges your tax strategy.

Sources & Further Reading:

- Internal Revenue Service (IRS) Publication 946: How To Depreciate Property

- Internal Revenue Service (IRS) Publication 463: Travel, Gift, and Car Expenses (Section 168(k) updates)

- The One Big Beautiful Bill Act of 2025 (P.L. 119-21) — Reinstatement of 100% Bonus Depreciation

Former CEO of a dozen-location gas station operating company. 180+ stations sold. Specializing in NNN gas station brokerage, sale-leasebacks, and investment sales across Florida and the Southeast.